The EU CBAM framework has entered a key new phase, with April 2026 deadlines and the first CBAM certificate price giving businesses a clearer picture of future compliance costs. Importers now need to focus on Authorised Declarant Status, supplier engagement and financial forecasting ahead of full implementation.

Share

Container Ship

The EU Carbon Border Adjustment Mechanism (CBAM) entered definitive implementation in January 2026, with major April milestones now shaping how obligated businesses prepare for future compliance costs.

With the European Commission publishing its first quarterly CBAM certificate price at 75.36€, businesses can now begin forecasting their financial exposure for imported carbon-intensive goods. But what happens next for importers that still need to secure Authorised Declarant Status or prepare supplier verification data?

This blog explains the latest CBAM developments, what they mean for obligated businesses, and how companies can begin preparing for future compliance costs.

You can find full details on the EU CBAM framework via the European Commission.

What is EU CBAM?

The EU Carbon Border Adjustment Mechanism (CBAM) applies a levy on carbon-intensive imports to tackle “carbon leakage”. This happens when businesses relocate production to countries with weaker carbon regulations.

The framework entered definitive implementation in January, with key milestones in April for obligated businesses relating to Authorised Declarant Status and certificate pricing.

For further guidance on CBAM obligations, visit the European Commission CBAM portal.

Authorised Declarant Status updates

From 1 January 2026, CBAM-obligated companies are required to apply for Authorised Declarant Status. This acts as the official registry of approved businesses permitted to import carbon-intensive goods into the European Union.

An initial deadline of 31 March 2026 was set for the submission of Authorised Declarant applications. Obligated businesses that applied before the deadline can continue importing CBAM goods while they wait for a final decision on their status.

However, businesses that have not yet secured this status can still apply but cannot import more than 50 tonnes of CBAM goods until approval is granted. Processing times published by local authorities can reach up to 120 days, making early application essential.

Applications must be submitted via the EU CBAM portal and require detailed information, including:

After submitting an Authorised Declarant application, businesses should begin forecasting their future CBAM compliance costs ahead of payments next year.

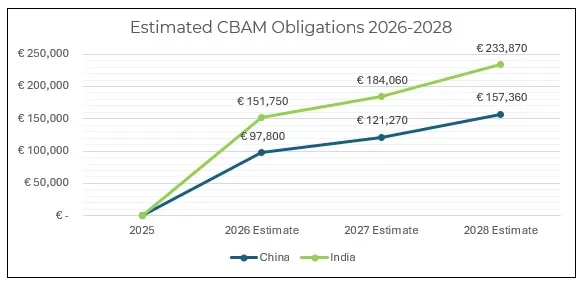

The European Commission published its Q1 2026 CBAM certificate price this month, set at 75.36€. Obligated businesses can now estimate their financial exposure under a worst-case scenario where they rely entirely on default emission values.

For example, importing 600 tonnes of goods under CN code 7208 from countries such as China or India could result in substantial compliance costs based on projected full-year EU ETS prices of:

75€ in 2026

80€ in 2027

90€ in 2028

Estimated obligations

Country of origin

Tonnage

2026

2027

2028

China

600

€97,800

€121,270

€157,360

India

600

€151,750

€184,060

€233,870

Cost estimates based on default values are typically higher and highlight the financial risk of relying on these values. They also demonstrate how costs can vary depending on the country of origin due to differences in default embedded emissions factors.

The latest EU ETS pricing information can also be found through the European Commission.

Why supplier engagement is essential

Obligated businesses should begin engaging with suppliers as early as possible to assess verification readiness.

This will become increasingly important ahead of the European Commission’s publication of its list of accredited third-party verifiers later this year.

Early preparation, accurate data collection and proactive supplier engagement will be critical to:

Not sure what packaging data you need to collect for EPR? This practical guide explains exactly what to report, including materials, packaging types, household vs non-household classification, and reporting deadlines, along with the most common mistakes UK businesses make.

The government portal ‘Report Packaging Data’ (RPD) online enrolment is now open for producers. Read our blog to find out what you must do and what resources are available to help guide you through this process.

Key takeaways from Interpack 2026: how the PPWR is shaping packaging innovation, circular economy collaboration, and future-ready compliance strategies.